From the companies beaten into bankruptcy by the pandemic and those that rose to new heights, to the rise of the SPAC and the spectacular collapse of a European tech company, KCM takes a look back on some of the biggest stories in business this year.

1. Riding the Stay-At-Home Wave

Zoom: This time last year, most people — aside from a small sliver of corporate America — hadn’t heard of Zoom. But that’s all changed thanks to the pandemic. The video conferencing app has emerged as the go-to platform for everything from office meetings to virtual Thanksgiving dinners. And its remarkable rise is made clear in its earning reports. During the first quarter, the company’s revenue soared 169% compared to the year prior, and 355% in the second quarter. Its shares have risen close to sixfold this year, making it a clear corporate winner amid the shift to remote work.

Peloton: In May, Peloton’s CEO John Foley made a bold pronouncement. As other companies were limping through the pandemic, Peloton, with its $2,000 stationary bike and streamed fitness classes, was uniquely tailored to thrive in our new stay-at-home world. While announcing that sales were up 66% and that the company had almost doubled its number of subscribers, Foley called Peloton “Covid-proof” and “recession-proof.” (paywall)

The company most recently announced its $420 million acquisition of Precor, an exercise equipment maker, in a bid to handle the increased demand for their bikes and treadmills.

Shopify: When the pandemic finally forced small businesses to open online stores, many of them turned to a somewhat obscure Canadian e-commerce platform, Shopify. In the second quarter, as retailers rushed to create an online presence, Shopify’s revenue nearly doubled to $714.3 million. The surge in new business led shares in the company to more than double this year, pushing its market value to roughly $117 billion — more than eBay and Target combined. (paywall)

2. The rise of the SPAC

In 2020, funds raised through special-purpose acquisition companies, or SPACs, surged to $73 billion. That’s nearly five times what was raised last year, leading a team at Goldman Sachs to dub 2020 the “year of the SPAC.”

The SPAC is a shell company created to raise money through an IPO and to then merge or acquire a private company. This year, the largest SPAC on record — Pershing Square Tontine Holdings — raised $4 billion. The craze even swept up Shaquille O’Neal, who teamed up with Martin Luther King Jr.’s son and three ex-Disney executives, to close on a $300 million SPAC.

Some high-profile companies, including DraftKings and Nikola, went public this year through SPACs, and Goldman predicts the trend will continue into 2021.

3. Taking tech public

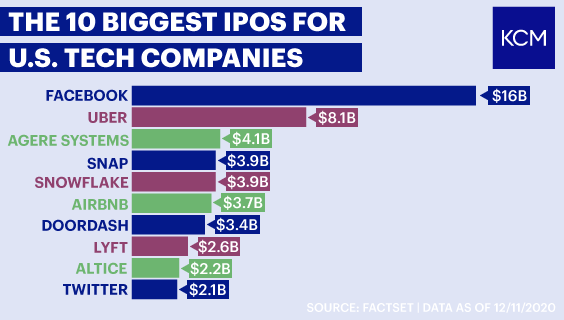

Three of the 10 biggest tech IPOs for U.S. companies unfolded this year.

In September, cloud warehousing company Snowflake made its highly anticipated market debut. The company had boasted revenue that grew over 130% in the first half of 2020, and revealed in the run-up to its IPO, Warren Buffett’s Berkshire Hathaway and Salesforce had each agreed to buy $250 million of its stock. When it went public, shares rose 111% and by market close, Snowflake — which was valued at $12.4 billion in February — was worth $70.4 billion. It was the largest ever software IPO, raising $3.9 billion.

In December, DoorDash raised $3.4 billion in its IPO. Shares rose 86% in the first day of trading for the food delivery company, which saw its third-quarter revenue spike with more people opting for takeout through the pandemic. (log-in needed)

The following day, Airbnb enjoyed a similar IPO pop, with shares rising 112% in its debut. The home-rental company had a turbulent 2020, slashing 25% of its workforce and postponed going public as the pandemic devastated the travel industry. But its successful IPO, which raised $3.7 billion, marked a stunning comeback for the company.

4. Retail bankruptcies

It’s been a bleak year for the retail industry. Lockdown restrictions kept some stores closed for months and business still remains sluggish. According to S&P Global Market Intelligence, there have been 49 bankruptcies as of mid-November, the most since the financial crisis slammed the sector.

Here’s a rundown of some of the biggest bankruptcies:

JCPenney: The department store chain founded over a century ago filed for bankruptcy on May 15 with 85,000 workers, more than 800 stores and nearly $5 billion in debt. J.C. Penney was purchased in November for $1.75 billion by Simon Property Group and Brookfield Asset Management, the country’s largest mall owners and emerged from bankruptcy this month.

Neiman Marcus: The luxury department store filed for bankruptcy protection in May and emerged from the process in September under a restructuring that eliminated $4 billion in debt.

Lord & Taylor: The country’s oldest department store is going out of business, closing all of its 38 stores.

Ascena: The parent company operating Ann Taylor, LOFT, Lane Bryant and Justice, filed for bankruptcy in July and planned to close 1,600 stores. A deal was struck this month to sell the brands to a private equity firm.

Guitar Center: The country’s largest seller of musical instruments, with more than 300 stores, filed for bankruptcy in November, and has emerged with a plan to shed $800 million in debt.

J. Crew: America’s iconic preppy clothing brand filed for bankruptcy in May and exited the process in September under new ownership.

5. A Spectacular Fraud

The remarkable unraveling of Wirecard, a German financial tech company once valued at $27 billion, is one of the largest and most intriguing cases of corporate fraud in years. Months of dogged reporting by the Financial Times revealed the company’s questionable accounting practices, but Wirecard was dealt its final blow in June when an audit found that $2.1 billion on the company’s balance sheet was missing.

Days after the finding, the fast-growing online payments business acknowledged that money likely doesn’t exist. Shares of the company immediately tanked, it was thrown into insolvency and its CEO and other high-ranking executives were arrested for fraud committed through a sprawling overseas network. Authorities in Europe and abroad have been on the hunt for the company’s Chief Operating Officer Jan Marsalek, who was added to Interpol’s most wanted list this summer after allegedly faking his entry into the Philippines, and is still missing.

6. The Year’s Biggest M&As

Here’s a look back at some of this year’s biggest mergers and acquisitions, from Slack to Grubhub.

Morgan Stanley — E*Trade: In February, investment bank Morgan Stanley agreed to pay $13 billion to buy discount brokerage E*Trade in the largest takeover by a U.S. bank since the financial crisis. (paywall) E*Trade brings with it 5 million retail customers and $360 billion in assets.

Morgan Stanley CEO James Gorman said he’d been eyeing the online brokerage for years before an opening appeared in 2019 when E*Trade’s two main rivals Charles Schwab and TD Ameritrade announced their own merger, leaving the company suddenly vulnerable.

Salesforce — Slack: Salesforce, the cloud-based software behemoth, in December said it struck a $27.7 billion deal to purchase workplace messaging app, Slack. Salesforce co-founder and CEO Marc Benioff called the acquisition a “match made in heaven.”

“Together, Salesforce and Slack will shape the future of enterprise software and transform the way everyone works in the all-digital, work-from-anywhere world,” he said.

S&P Global — IHS Markit: The year’s biggest acquisition belonged to S&P Global, which owns indexes like the Dow and S&P 500. The company agreed to pay $44 billion to buy IHS Markit, a transaction that would create a financial information powerhouse.

Intuit — Credit Karma: Intuit, which makes TurboTax and QuickBooks, purchased Credit Karma for $8.1 billion. Intuit CEO Sasan Goodarzi said their interest in the startup was for its reach (110 million members) and its data. Credit Karma provides free credit score tracking and products like credit card and loan comparison tools, and a tie-up would strengthen both companies’ offerings.

Grubhub — Just Eat Takeaway: In June, European food delivery giant Just Eat Takeaway — itself the product of a merger this year — announced it’s buying U.S. rival Grubhub for $7.3 billion. The deal follows Uber’s failed takeover attempt earlier this year, an acquisition that would have formed America’s largest food delivery service.

Uber instead turned its attention to Postmates, which it bought this summer for $2.65 billion.

Written and reported by Rachel Uda.